Drive Shack, formerly Newcastle Investment (NCT), is a golf management company. The original thesis for Drive Shack (DS) and valuation is here . When I first bought it ~$3/share, the thesis was that there were forced sellers due to cancellation of dividend and REIT status. Add to it the headline risk of "Golf is declining". I was happy to buy from these forced sellers.

Since then, the stock price has gone up ~70% after Wes Edens increased his ownership to 9%, buying $2.5M of stock at $6 / share. While Wes Eden's buy is a good sign, there are several other developments which require a revision to the original thesis. As announced in Q417 earnings call, the company is transitioning away from being owner of traditional golf courses to development of Topgolf like golf entertainment sites. So I want to look at it as a development company and an example of balance sheet to income statement investment.

Some key recent developments are:

Let's examine the management plan to sell owned courses:

DS claims that they can sell their owned golf courses for 8x - 10X EBITDA plus added premium for CA. They estimate that they can sell their owned golf courses for $200M - $325M, minus $100M debt, leading to Net proceeds $100M to $225M.

DS claims that they can sell their owned golf courses for 8x - 10X EBITDA plus added premium for CA. They estimate that they can sell their owned golf courses for $200M - $325M, minus $100M debt, leading to Net proceeds $100M to $225M.

Let's try to assess these golf course valuation estimates with other recent transactions:

a. Chinese buyers

In 2016, HNA Holdings (Chinese conglomerate) bought 10 golf courses in 5 Puget Sound counties for $137.5 million (1880 acres) from Oki golf as part of sale and leaseback transaction.

b. Private Equity buyers

Apollo bought Club Corp at 7.5x 2018 EBITDA in 2017 ( https://bloom.bg/2t4Ksxx )

c. Residential developers

The Carmel Highland Golf Course in Rancho Penasquitos, which closed in 2015, was sold a year later for $14.5 million to a developer who plans to build housing on the 114-acre site. This implies valuation of $120K / acre.

One caveat here is that redeveloping golf courses for housing in CA is hard due to NIMBY opposition. For example, Escondido golf course was zoned for residential development but still took ~5 years to start development, while Poway golf course was zoned for open space/recreation and residents voted against changing part of the course zoning to residential for condo development.

If we take the $72K / acre valuation from the Oki golf sale and add 20% California premium for the 14 DS CA golf courses with ~2000 acres, we get valuation of $172M. Let's assume that the non CA courses produce $10M EBITDA and assume 8x EBITDA multiple (similar to Club Corp deal), we get valuation of $80M for non CA courses. So total valuation of $252M for all owned golf courses, close to the mid point of what the company gave as valuation range ($200M - $325M). This validates the company estimate of $300M cash that they can then pour into constructing Drive Shack locations.

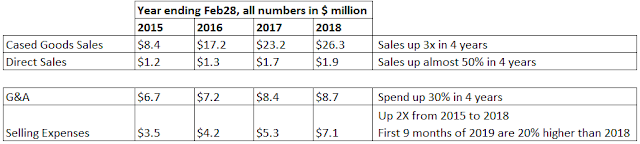

Here's what the company thinks the Drive Shack locations should be valued at (h/t @KonekoResearch twitter post for table below):

Here's what the company thinks the Drive Shack locations should be valued at (h/t @KonekoResearch twitter post for table below):

To validate management projections for Drive Shack concept, it will be useful to look at projection from rival Topgolf. From https://bloom.bg/2oWnTvM, Topgolf says it takes $20M - $25M to construct each site, revenues are 15-20mm/facility and the EBITDA margin is 40% (this EBITDA margin number is on various websites but could not find a source attributable to Topgolf executives quotes). These numbers provide good support for management numbers on cost and EBITDA per site. Drive Shack has the second follower advantage here and they can just copy what works at Topgolf, thereby reducing risk.

I doubt that the market will value it at 20X EBITDA (nice try, Drive Shack CEO!). 10X -15X EBITDA seems more reasonable given the growth rate, and leads to range of values from $11 /share to $16 / share which is lot higher than current share price in $5 range. Getting to 15 Drive shack locations can take between 1.5 to 3 years, so a 3 year time horizon seems the right way to view this investment.

Its important to note that there is additional value above $11 - $16 / share from these factors:

1. Managed / leased golf courses could be worth $100M - $200M (4X - 8X EBITDA multiple) which is additional $1.6 - $3.3 / share

2. The company will have unlevered balance sheet in the valuation case discussed here. There will be additional ways to unlock value such as taking on some debt, buying back stock, instituting a dividend etc. Hard to put a number on it though.

Risks:

1. Its possible Drive Shack concept fails, and cannot copy what Topgolf has done. Topgolf has proven the concept, so its really a matter of choosing the right site and then copying what works at Topgolf. Let's say that Drive Shack still fails in copying Topgolf due to unproven / unskilled management, and the first 5 sites are closed. I think there's still enough downside protection even in this case. If first 5 sites are shut down, Drive Shack will have cash of ~$200M (this is from wind down of legacy assets + Sale of golf courses - $100M cost of building 5 Drive Shack sites). The managed golf courses are worth $100M - $200M. So total valuation of $300M - $400M ($ 4.5 - $6 / share). This means that there's downside protection at current share price of ~$5/ share.

2. The sale price of CA owned golf courses is lower than estimated here. This is possible but low likelihood because DS has the time to sell the owned golf courses either piecemeal or as a packaged deal, and they can wait to get the best price from the potential buyers (Chinese buyers, PE, or real estate developers).

3. Recovery from legacy RE assets is less than $75M estimated by management.

No comments:

Post a Comment