Antero differs from the other stocks I typically write about or invest in, because:

1. It's not a small / micro cap stock, and is covered by several Wall Street firms,

2. It's in the commodity segment. And I have no special forecasting capability on the price of natural gas (But does anyone else, really?)

Yet I still invested in Antero because I believe it's undervalued. I first bought small position in $AR in mid 2016. The thesis was simple: the market was valuing Antero only for the drilled acreage, and was valuing undrilled acreage at zero. Plus, Antero owns contiguous acreage in the prolific Marcellus shale which allows for longer laterals. Recently, SailingStone Capital which owns 11% of $AR stock gave the same thesis on Antero in a letter to the Board: "The shares of Antero Resources trade at a discount to the value of the company’s proved reserves using the futures strip and a 10% discount rate, and reflect no value for the company’s vast acreage position and liquids-rich drilling inventory in the Marcellus Shale."

Since 2016, the stock moved slightly down. Despite this, I've recently added substantially more to this investment to make it a mid-sized position (5%), and this post will provide an updated thesis. I can't predict when AR stock price will move up, but what I know is that Antero is undervalued and value is being created, and it will be realized someday.

Let's start the thesis by looking the "bad" side of Antero

There are two frequently cited items here:

1. Complicated corporate structure,

2. Abundant natural gas in US, with potential impact of low natural gas pricing for long period

The corporate structure is complicated and major investors have written letters asking the Board to simplify the structure. Chapter IV sent a letter to the Board explaining why they exited the investment due to complex corporate structure. SailingStone Capital also wrote a letter (Exhibit D in this filing) asking the Board to evaluate options such as share buybacks, reducing debt and simplifying corporate structure. The Board is currently doing a strategic review, but my overall thesis does not depend on the outcome of that review.

The complex organization structure is shown in the figure below. The Sponsors are PE firms (Warburg Pincus, Yorktown) and management (Rady and Warren). A common criticism with this complex structure is that Sponsors profit from being owners of the GP, and profits for GP ($AMGP) increase faster than those for LP. This leads investors to suspect that the drilling program is driven mainly for the purpose of increasing GP profits. Another angle here is to look at how much money Sponsors have tied up in each of the companies in the structure. Sponsors own $1.8B of $AMGP stock and $1.5B of $AR stock. I'd argue that Sponsors have put roughly the same amount of money into AR and AMGP, and I don't think their interests are heavily skewed towards the GP at the expense of AR, especially when considering that AR is quite undervalued (more on this later).

I don't believe that rising GP profits are the main motive for the drilling program. Instead, I believe the major reasons are:

1. Management (which owns 9% of the stock) believes that it is a good investment to keep drilling,

2. AR has higher firm transportation capacity than current production, which means they are taking a loss due to take-or-pay agreements with pipelines. They are losing about $0.16 per Mcfe due to excess capacity.

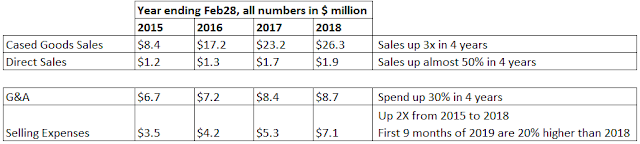

3. AR can lose their lease on acreage if there's no production by a certain date, see table below for example.

The big questions are:

What is the economic reality at AR? Are they spending cash today to create wealth, or are they sinking cash (i.e. destroying wealth) with their drilling program?

The full cycle rate of return is 28% (source: 2018 Analyst day) which is lot higher than cost of capital, and so drilling program is creating wealth. Of course, Antero could slow down the drilling program, and sell their finite reserves of natural gas at higher prices in the future. This needs to be balanced with not losing acreage due to no production. I don't know what the sweet spot is for not losing acreage vs not selling too much gas at low prices.

Unit economics is another useful way to look at E&P companies. Antero has cash margins of $1.13 per Mcfe for 2018. However, they are losing $0.16 per Mcfe due to take-or-pay on firm transportation. As Antero grows production, there will be two upsides: a. loss on transportation will go away, pushing cash margins upto $1.4 per Mcfe, b. G&A costs will be spread over larger revenue.

Valuation:

If we subtract $AM holding from $AR's market cap, the market is pricing stand alone E&P at $2.8 Billion. 2018 Operating Cash Flow is estimated to be $1.5 Billion , and maintenance capex is ~$580 Million (source: 2018 Analyst day). So excluding growth capex, cash flow is $0.9 Billion. $AR has net operating loss of $3 Billion at federal level and won't be paying taxes for a long time. That's yield of 32%. Even after using up or expiring NOLs, they'll have $0.7 Billion of cash flow (Excluding growth capex) which is 25% yield.

Additional considerations that enhance value:

1. E&Ps get tax shelter through expensing of Intangible drilling costs. I find this example of tax shelter at work interesting: though Antero received cash proceeds from derivative monetizations of $750 million in 2017, their NOLs increased by $1.6 Billion.

2. Antero has liquids rich portfolio. So there's potential upside if oil prices go up.

3. Antero has a large hedge book that will help them through periods of low natural gas prices.

Additional Reading:

1. My twitter thread on shale oil vs shale gas

2. Excellent VIC writeup on Antero

3. Antero Analyst day 2018 slides

4. Full cycle vs half cycle rate of returns for oil and gas

5. David Einhorn presentation on shale gas

6. Brief explanation on Intangible Drilling Cost and tax breaks